On february 2023, Fair Finance Guide Japan (FFGJ) published the report “Reckless Investments by Son Masayoshi (Softbank) Swells Informal Economies in Asia” (in Japanese).

Below is a summary. The full report (in Japanese) and the English summary of the report are available on FFGJ’s website: https://fairfinance.jp/bank/casestudies/rideshare2023/

Ride-sharing apps which allow users to have a car pick them up at almost any location and take them to their desired destination with just a couple of taps on the app, are expanding their businesses globally. The market is estimated to have been worth $76.48 billion in 2020 and it is estimated that it will continue to grow and reach $242.73 billion by 2028. At first glance, this fast-growing industry appears to be a prime investment destination, and large amounts of investment have already been made from Japan and the rest of the world, pushing the ridesharing industry even further into a growth industry.

However, the industry is transforming the social and economic situation of local transportation systems, and the following problems have been pointed out:

Ride-sharing is not what it claims to be

While claiming to be a platform for matching users who wish to head in the same direction/destination, an Indian survey shows that 94.6% of drivers who register as drivers earn their income by working more than 8 hours a day on ride-share apps. This means that most workers are engaged with the app to generate their primary income, rather than supplementary income. These drivers are not “sharing” a trip to the station. They have no business at the destination. The app is thus used primarily as a vehicle dispatch app, rather than pursuing the economic rationale of a “sharing economy” by coordinating rides. Yet, the companies involved have shown very little interest in adjusting its operations to fit this reality. In fact they have shown themselves to be ill-prepared to take corporate responsibility towards its drivers.

Ride-sharing encourages the informal economy

The entry of ridesharing services is hurting the existing cab industry and forcing it to restructure in various countries. In Vietnam, for example, about 34,000 people from the two largest existing cab companies have lost their jobs. Although many of these workers are believed to have become rideshare drivers after losing their taxi jobs, rideshare drivers operate in the informal economy. Even if they were able to earn some significant level of income, they were still forced to move from the formal economy to the informal economy. Even if drivers are able to enter into some contractual relationship, supreme court cases in France and Great Britain have ruled that they amount to fraudulent contracts meant to avoid regular employment of workers. In countries that have not yet gone that far, drivers still often times lack employment insurance, workers’ compensation insurance, and healthcare according to a study conducted in India and by testimonies in other countries.

Exploitation and tax evasion enables predatory pricing

Ridesharing companies are able to provide services at excessively low prices, so much so that it is often times referred to as “predatory pricing”. This is partly due to the companies not hiring drivers as regular employees as mentioned above. One thing this allows app providers is to reduce social security costs. But on top of that, the app providers also attempt to avoid taxes by registering as something other than the taxi industry (for example, IT companies). These measures often end up being shot down by the court as illegal classifications. However, by the time court cases are settled and the companies are ordered to pay additional taxes, the taxi industry and its workers will have already suffered a major, and sometimes irreparable, blow.

Initial investments are not for system development, but for lobbying and legal fees

The programs and systems involved in rideshare apps are mostly developed and actually do not require too much additional investment. The initial investment in rideshare app providers are thus used for cash backup to provide predatory pricing. This allows app providers to destroy competitors. The investment is also used for lobbying and lawyer fees to either retroactively legalize malpractice or to prolong the court cases so as to give them time to profit off of shady business practices.

Driver compensation is drastically cut down once competition is decimated

After competition in the taxi industry has been all but destroyed, compensation for rideshare drivers are drastically cut. Throughout Asia, drivers testify that “things were only good in the beginning”. In Indonesia for example, per kilometer compensation has been reduced from the initial 4000 rupiah per kilometer to 1600 rupiah per kilometer. This has made it difficult for drivers to secure an income equivalent to Jakarta’s minimum wage. Workers in India also testified that their income has dropped from earning over 70,000 rupees per month to less than 30,000 rupees per month. Many workers are forced to work long hours to make up for this cost-cutting. A survey in India indicate that as many as half of them work more than 14 hours per day.

Most importantly, these problems are not isolated to individual countries. Similar problems have been identified around the world. While problems are duplicated, there has been no sincere response on the part of app providers. Rather, if we consider this in light of the statements made by Travis Kalanick, the founder of the leading company in the industry, Uber, we can say that this repetition of the same problems is rather intentional. The business model is designed to: 1) provide services at low prices by depriving drivers of their rights and using tax breaks of questionable legality; 2) once they dominate the market; profit margins are increased by cutting compensation to drivers, sometimes by half or less, 3) hire an army of lobbyists and lawyers to stall the legal process; and 4) use the few years they have before the law and regulations catch up to recover investments and make profits.

This whole scheme is contrary to the ILO Declaration on Fundamental Principles and Rights at Work and to SDG target 8.3, indicator 8.3.1, and target 10.2. It is a mass production of informal employment with inadequate social security, which hinders the meaningful economic and social inclusion of many workers.

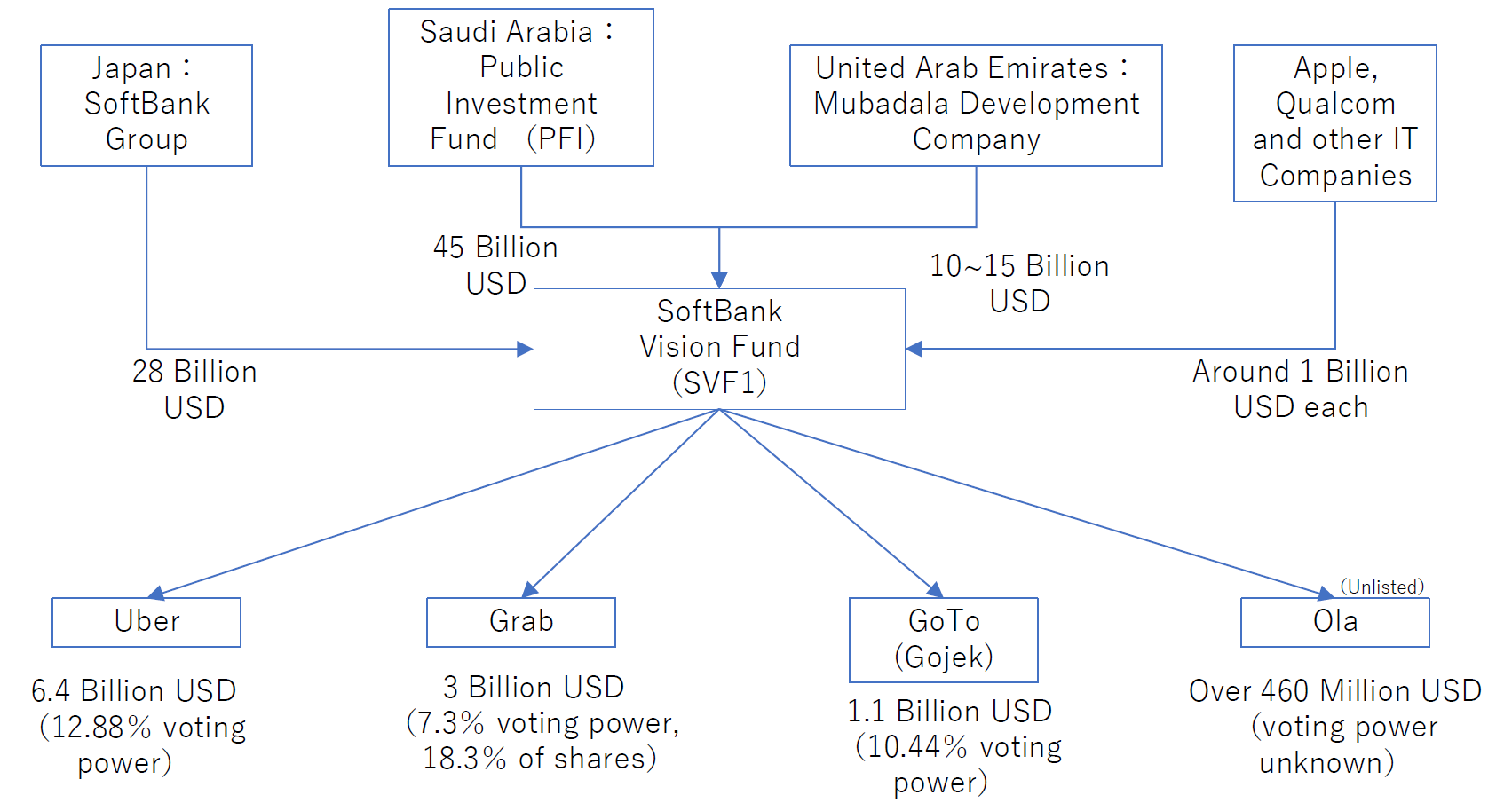

The industry is supported by massive investments, and the single large shareholder that is found to have been investing in most major ride-sharing companies in Southeast Asia and India is the SoftBank Vision Fund, managed by the SoftBank Group of Japan. SoftBank Group is thus the investor most financially involved in the rise of ridesharing and its disruption of the labor market in Asia. They are the principle external shareholder in at least three of the largest rideshare app providers (Uber, Grab and Gojek), and is likely one of the primary investors for Ola.

However, despite the growth of rideshare apps in Asia, the fund has actually been questioned for its risk-averse stance and has in fact reported large losses in 2022. Two things are supporting such investments by the SoftBank Group. One is a $45 billion investment from the Public Investment Fund (PIF), the Saudi Arabian sovereign wealth fund. This fund is under the direction of Crown Prince Mohammed Bin Salman, who is believed to be involved in the murder of U.S. journalist Jamal Khashoggi. If profits are simply allocated according to the percentage of investment, it can be said that PIF and thus Muhammad Bin Salman would benefit the most if the SoftBank Vision Fund were to turn profitable in the future.

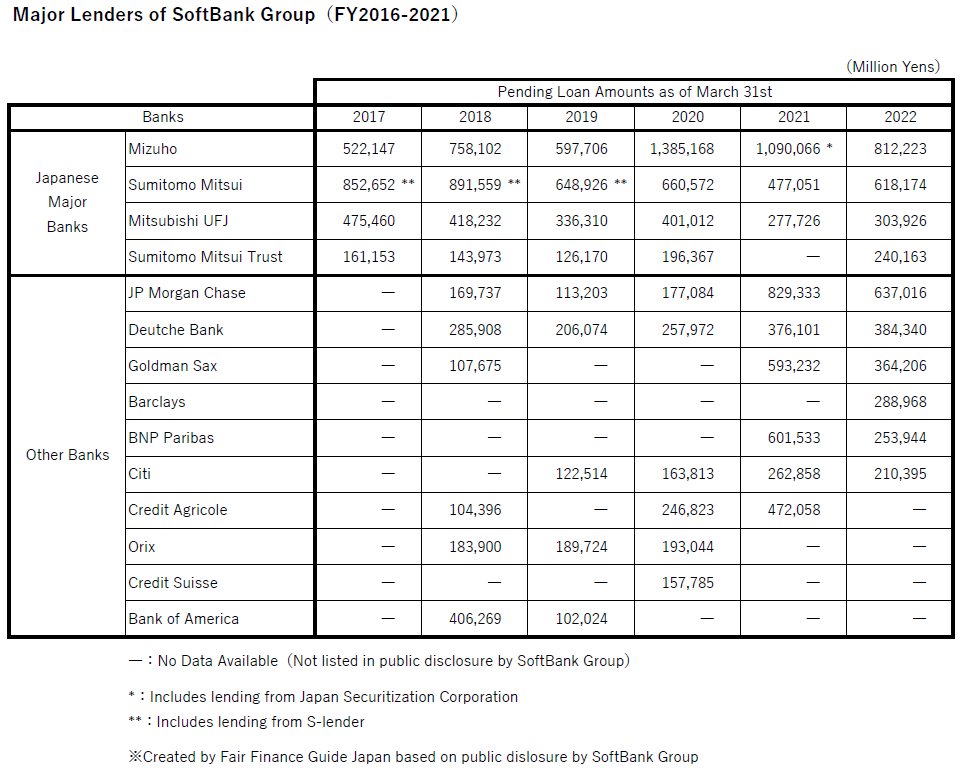

The other thing that allows SoftBank Group to make risky investments is the lending by domestic and foreign financial institutions. Among these, Mizuho Financial Group has single-handedly lent more than 1 trillion yen to the SoftBank Group and has had an extensive “honeymoon relationship” with the group since the founding of SoftBank. It is even said within the industry, that Mizuho “seems to offer extremely lenient screening and interest rates” for SoftBank. In that sense, Mizuho is the financial institution most supportive of SoftBank’s CEO and founder Son Masayoshi and his ambitions.

In light of the already observable social impacts of SoftBank Group’s ambitious investments, Mizuho Financial Group needs to strengthen its due diligence. It should also consider the possibility of its business partners providing benefits to persons who are alleged to have ordered serious human rights abuses. Mizuho needs to strengthen its efforts to conduct appropriate engagement to prevent/mitigate this from happening.

Major Japanese banks do have human rights policies respecting the ILO Declaration on Fundamental Principles and Rights at Work, and major Japanese banks are signatories to the Equator Principles. The Equator Principles are a framework for financial institutions to evaluate and manage the financing of large-scale development and construction projects in developing countries to ensure that the environmental and social risks associated with such projects are fully understood and considered. Therefore, as signatories of the principles, banks must take note of workers’ rights in project finance in the Global South.

However, the Equator Principles framework does not apply to all corporate loans. It is only for loans tied to projects. In other words, the framework does not work for corporate loans to the SoftBank Group, which does not directly have large-scale development projects. Although nearly ¥2 trillion in loans from Japan’s major banks has allowed the SoftBank Group to invest recklessly, the current policy leaves the banks without any ethical basis to curb the problems caused by the Group’s reckless investments.

If the SoftBank Vision Fund continues to suffer significant losses, the banks may give up on it anyway, but they should expand the scope of their human rights policies before that happens. In order to protect the livelihoods and rights of workers in Asia.

Figure 1. Investments to Major Rideshare Companies in Asia from SoftBank Group